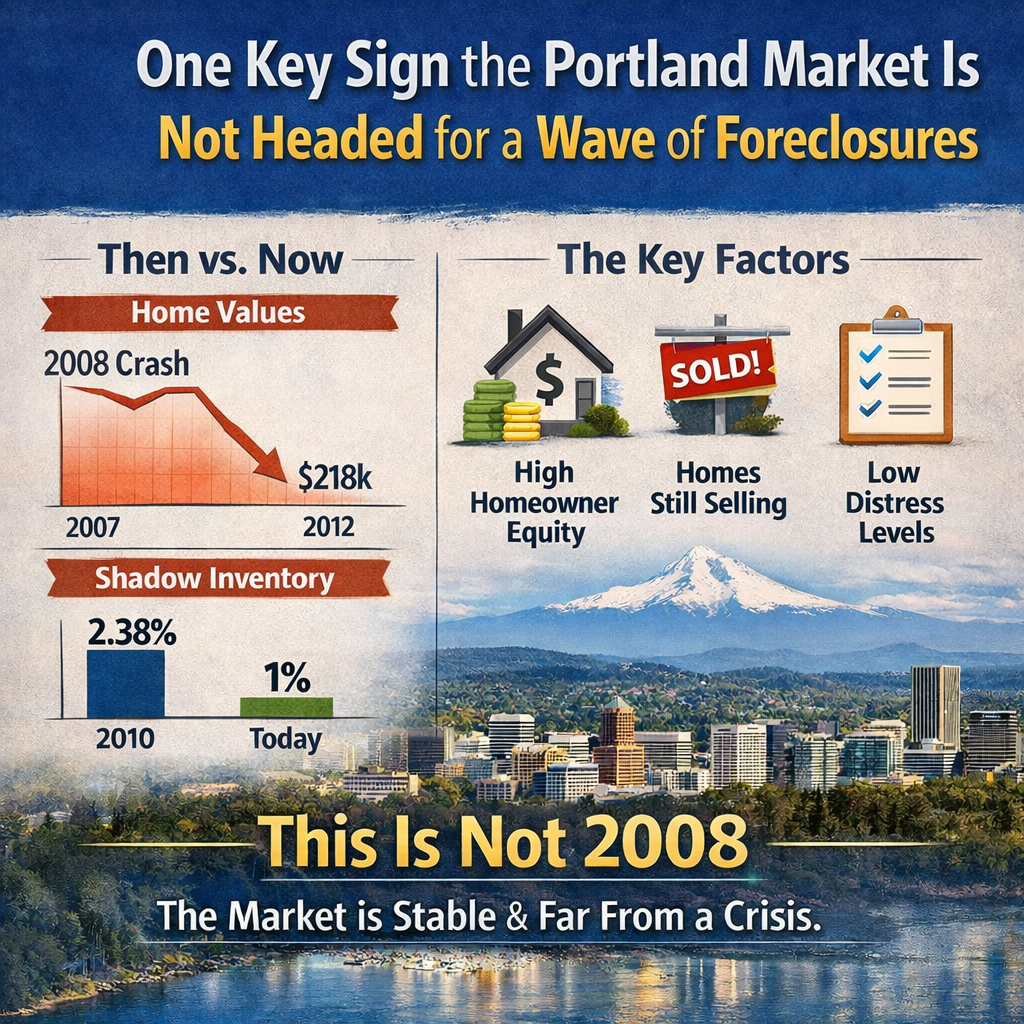

One Key Sign the Portland Market Is Not Headed for a Wave of Foreclosures Foreclosure…

The Truth About Housing “Crashes” in the Pacific Northwest

The Truth About Housing “Crashes” in the Pacific Northwest

Every few months someone pops up saying a housing crash is coming. It’s usually loud, dramatic, and packed with scary headlines. But here’s the truth: the Pacific Northwest market doesn’t behave like the national market — and it definitely doesn’t behave like 2008.

If you’re buying, selling, or refinancing in Oregon, Washington, or Idaho, here’s what you really need to know.

1. Today’s Buyers Aren’t 2008 Buyers

Back then, banks were handing out loans to anyone with a pulse.

Half of new mortgages were going to buyers with credit scores under 720.

Today?

Most borrowers are 720+, and a huge chunk are 760–800. These are strong, well-qualified buyers who can actually make their payments.

A crash needs mass defaults. We’re nowhere near that.

2. Inventory Is Still Tight — Even With Higher Rates

Could prices soften? Sure, in certain pockets.

But a crash needs oversupply, and the PNW has the opposite problem.

-

Oregon is still massively undersupplied.

-

Washington’s building pipeline hasn’t caught up.

-

Idaho slowed construction right when demand stayed steady.

Even when rates spiked, inventory didn’t surge.

Sellers don’t want to give up their 3% mortgages, so they’re staying put.

Low supply is a natural price floor.

3. Prices Already Corrected… Quietly

Here’s what most crash callers miss:

A correction already happened — it just wasn’t dramatic.

In many cities across the PNW:

-

Prices dipped 5–10% from the peak

-

Then stabilized as inventory tightened

-

Then slowly climbed again in 2024–2025

This is a normal cycle, not a collapse.

4. The PNW Drives Demand From Outside the PNW

We don’t live in a closed box.

Buyers come in from:

-

California

-

Seattle relocating to Portland suburbs

-

Remote workers chasing lifestyle upgrades

-

Retirees moving to Idaho

That “imported demand” props up the market even when locals feel squeezed.

5. Affordability Is the Real Issue — Not a Crash

This part is true:

Affordability is tough right now. Rates are high. Prices are high. And incomes haven’t kept up.

But affordability doesn’t create housing crashes by itself.

It creates:

-

Slower sales

-

Longer days on market

-

More negotiation power

-

More rate-dependent activity

None of those equal a collapse.

6. The Only Thing That Could Trigger a Crash? A Surge in Forced Selling

And we aren’t seeing it.

No wave of job losses.

No huge reset of risky loan products.

No meltdown in credit quality.

No flood of foreclosures.

In fact, delinquency rates are still low.

Until forced selling rises, there is no crash setup.

7. So Where Are We Headed?

Here’s the honest view:

-

We’re in a rate-driven holding pattern

-

Prices may move sideways in some markets

-

Strong pockets (Portland suburbs, Vancouver, Boise) will likely stay firm

-

When rates fall, buyer demand returns fast

The PNW is a supply-constrained market. That keeps it resilient.

Final Thoughts

Ignore the sensational crash headlines.

This isn’t 2008, and the fundamentals don’t support a collapse.

Related Posts