As we turn the page on 2025, the housing market in the Pacific Northwest is…

Portland Mortgage Rates: What Rising Inflation Means for Your Move

Portland Mortgage Rates: What Rising Inflation Means for Your Move

Short answer: Inflation rose to 3.8% in April 2026, so Portland mortgage rates are stuck near 6.5% and likely won’t fall soon. If you need to move, a smart plan beats waiting for lower rates that may never show up.

The latest data is not what buyers hoped to see. Inflation went up again, and that keeps Portland mortgage rates high. Before you panic over the headlines, here’s what is really going on — and what it means if you’re thinking about buying or selling in the Portland-Vancouver-Hillsboro area.

Why did inflation go up again?

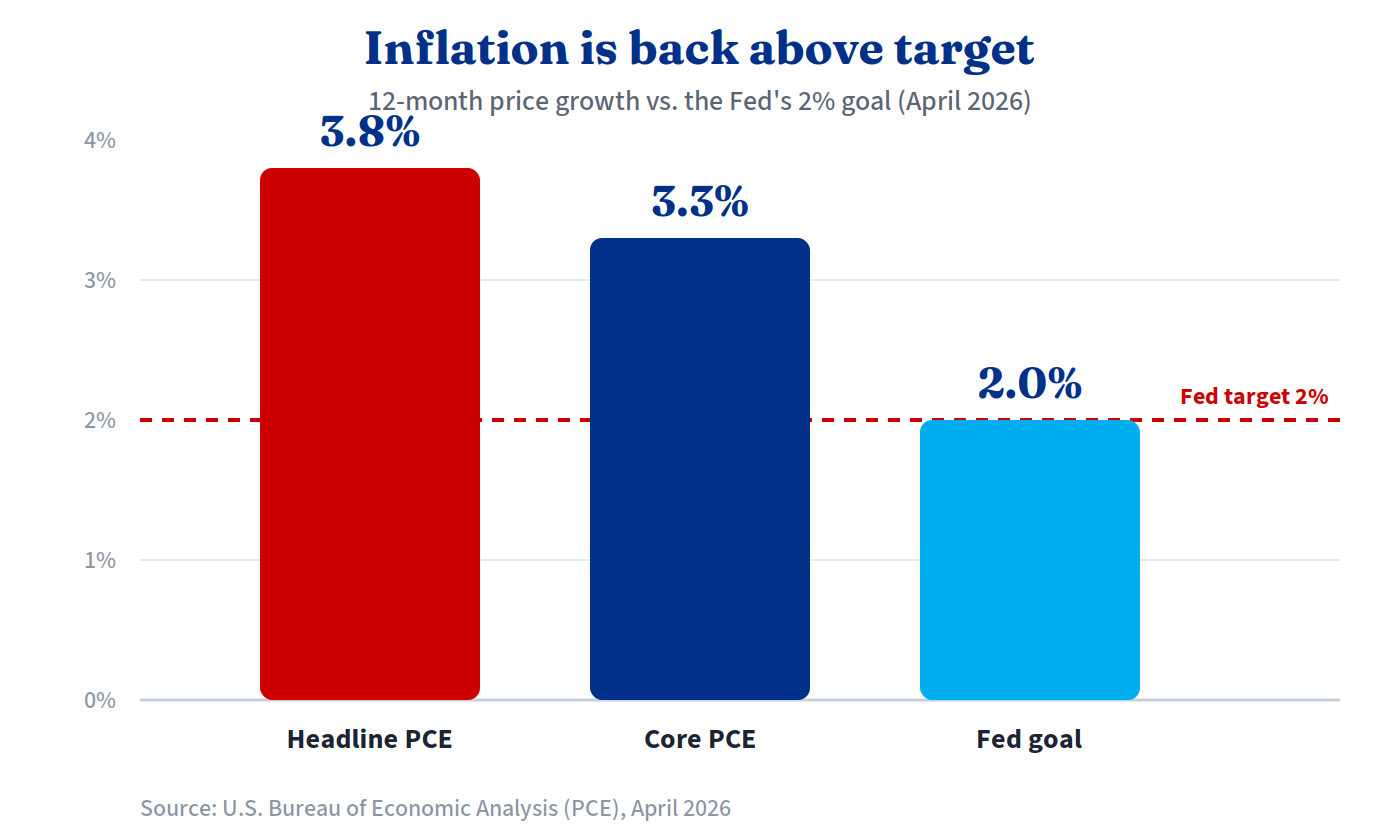

The government tracks prices with a tool called the PCE index. It shows how much more you pay now than you did a year ago. In April 2026, that number hit 3.8%. That’s the highest in about three years.1

A big reason is energy. The war in Iran pushed oil and gas prices up. That made many other goods cost more to make and ship. Higher energy costs mean higher inflation.

There’s a calmer number too. “Core” PCE leaves out food and gas. It came in at 3.3%.1 The Federal Reserve (the Fed) watches core prices the most, because gas prices swing around a lot. Core is high, but not as high as the headline number. That hints some of the spike is tied to oil. If the conflict cools, prices may cool a little too.

What does inflation mean for Portland mortgage rates?

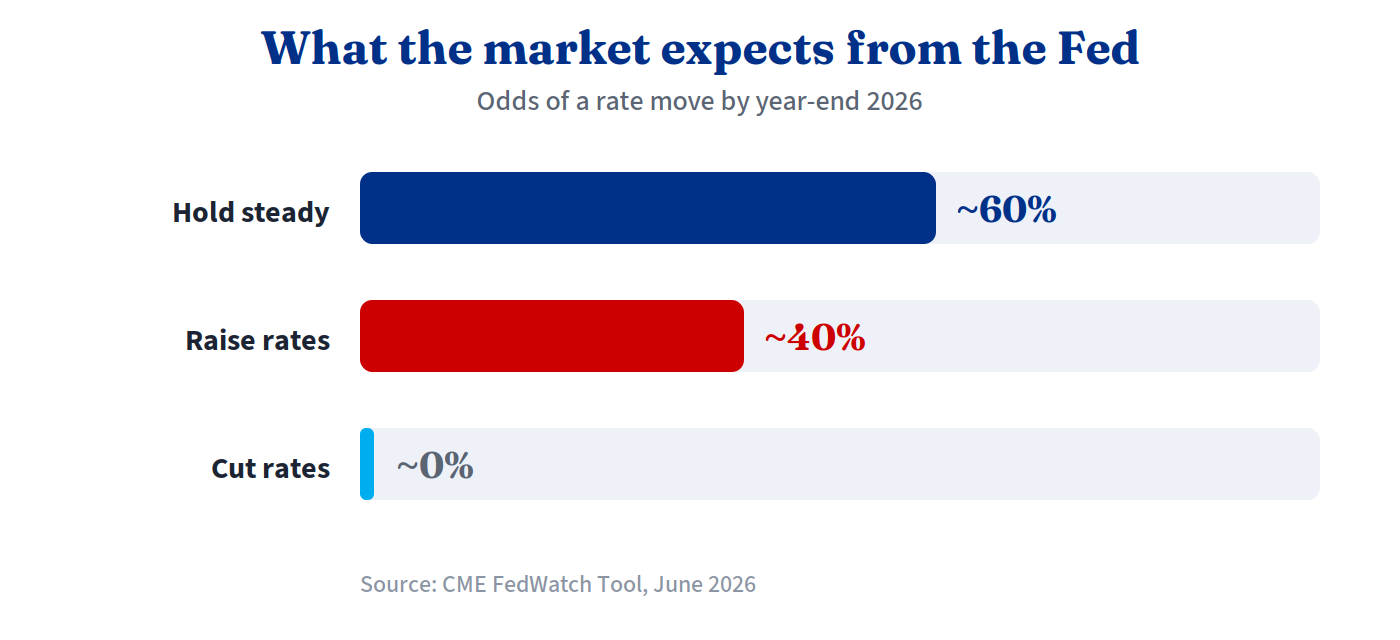

Here’s the housing link. When prices rise fast, the Fed keeps its key rate high to slow spending and cool inflation. That rate is not your mortgage rate. But over time, the two tend to move in the same direction.

Right now the Fed’s rate sits at 3.50%–3.75%. Markets expect the Fed to hold steady at its June meeting. But traders now see about a 40% chance of a rate hike before the end of 2026 — and the odds of a cut are close to zero.2

So Portland mortgage rates are likely to stay about where they are. As of early June 2026, the average 30-year fixed rate is near 6.5%.3 If you’ve been waiting for rates to drop a lot before you move, “higher for longer” is still very much on the table.

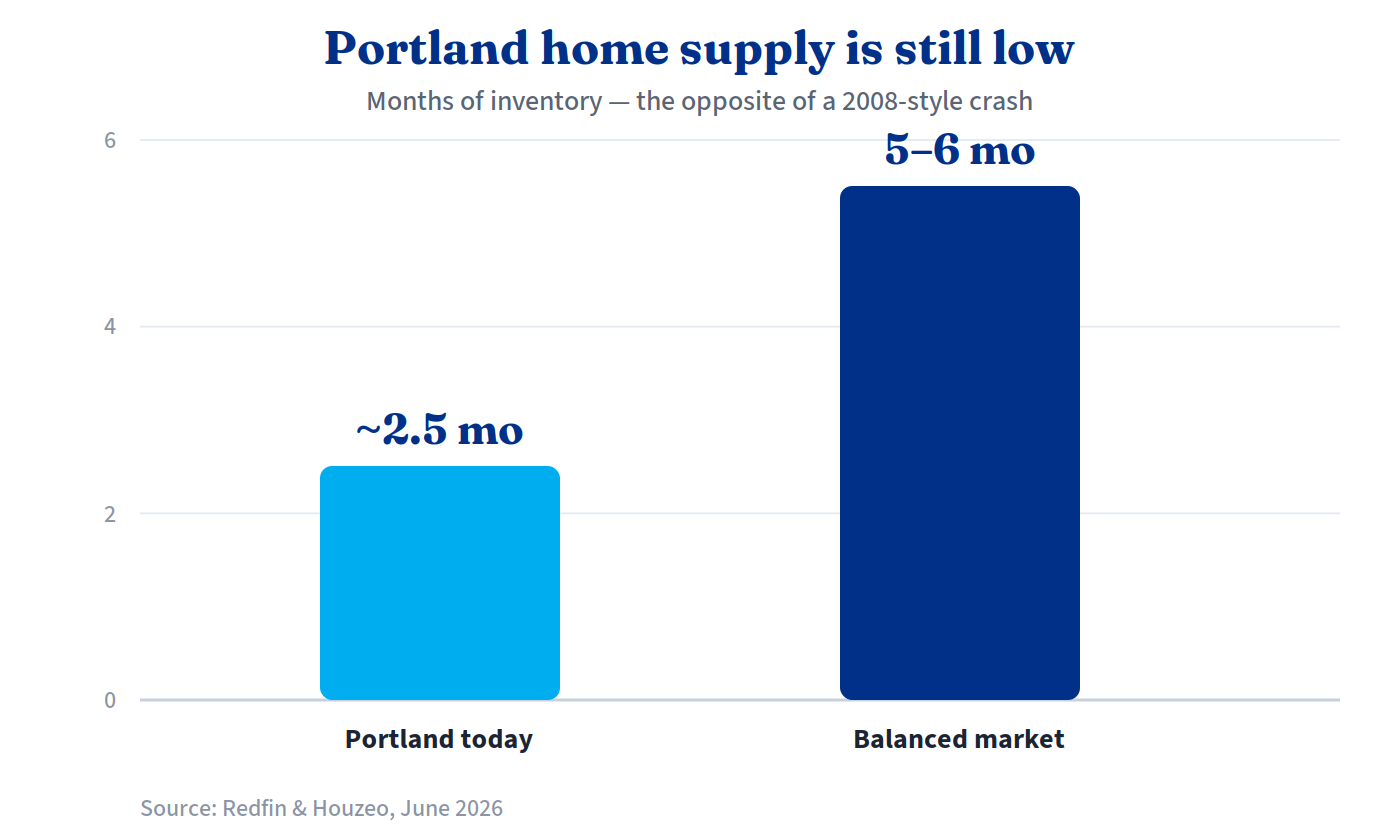

~2.5 months

of homes are for sale in the Portland area today. A balanced market needs 5–6 months. Low supply is the opposite of a crash.4

Is this another 2008 housing crash?

No. A hard market is not a crashing market. The setup today is very different from 2008. Back then, too many homes hit the market at once, owners had little equity, and loans were handed out too easily. Today is almost the reverse.

| What to watch | 2008 setup | Portland today (2026) |

|---|---|---|

| Homes for sale | Way too many | Low supply, ~2.5 months |

| Owner equity | Very low | Most owners hold strong equity |

| Lending rules | Loose and risky | Strict and careful |

| Main problem | A flood of forced sellers | Affordability, not a sell-off |

The hard part today is price and rate, not a wave of distressed sellers. Uncomfortable and unhealthy are not the same thing. The market feels tough right now, but “tough” and “crashing” are very different.

What are my options if I want to buy in Portland now?

High rates don’t put homeownership out of reach. The path just looks a little different. Here are real ways to make the numbers work:

- Ask about a temporary buydown. A 2-1 buydown can lower your payment for the first year or two while rates stay high.

- Look into first-time buyer help. Oregon and Washington both offer programs and down payment assistance.

- Ask for seller concessions. In a slower market, some sellers will help cover costs or buy down your rate.

- Get pre-approved first. When rates move — and they will — you want to be ready to act fast.

The right plan for your goals matters far more than waiting for a perfect moment that may never come.

Know exactly what you qualify for.

I’ll shop multiple lenders and show you a monthly payment that fits your budget — a local alternative to big retail names like Rocket and Zillow. Let’s build a plan that works for your move.

Matt Jolivette of Associated Mortgage Brokers · NMLS #90661

Bottom line

Inflation is still above the Fed’s goal, so Portland mortgage rates will likely stay high for a while. But if you need to move, strategy matters far more than trying to time the market perfectly. Cut through the noise, run your real numbers, and make a plan that fits your life.

Frequently asked questions

Will Portland mortgage rates go down in 2026?

Probably not by much. Inflation is high, and markets see almost no chance of a Fed rate cut this year. Most signs point to rates staying in the mid-6% range for now.

How much does a home cost in the Portland area right now?

The median home in Portland sold for about $512,000 in spring 2026, roughly flat from a year earlier. Prices in nearby Vancouver, WA are similar, in the high $400,000s to low $500,000s.5

Should I wait to buy until rates drop?

Maybe not. Rates may stay high for a while, and local home prices are stable, not falling fast. Waiting can cost you in rent and lost equity. A temporary buydown can lower your payment now, and you can always refinance later if rates drop.

How does a rate buydown work?

With a temporary buydown, your rate is lowered for the first year or two, then it returns to your normal fixed rate. That eases your monthly payment while rates are high. In a slower market, sometimes the seller or builder helps pay for it.

Is now a bad time to buy in Portland?

Not on its own. Low home supply means this is nothing like the 2008 crash. The real question is whether the monthly payment fits your budget. A quick pre-approval gives you that answer fast.

Disclaimer: This article is general information only and is not financial, lending, or investment advice. Loan approval is subject to credit, income, and property qualification. Rates and figures are accurate as of June 2026 and are subject to change. Matt Jolivette of Associated Mortgage Brokers, NMLS #90661, Company NMLS #86136. Equal Housing Opportunity.

Related Posts