Truck drivers are the backbone of the American economy. You spend long hours on the road, navigating complex routes, and ensuring that essential goods reach their destinations. However, when it comes time to park the rig and settle into a home of your own, you might find that traditional banks do not understand how you earn your living. From per diem pay and fluctuating mileage rates to 1099 independent contractor status and massive tax write-offs, the unique way truck drivers are compensated can make qualifying for a home loan feel like an uphill battle.

If you are a CDL professional looking to buy a home or refinance in Portland, Oregon, Washington, or Idaho, you need a mortgage broker who speaks your language. I am Matt Jolivette, a Certified Mortgage Consultant® (CMC®) with 25 years of experience at Associated Mortgage Brokers. I understand the nuances of trucker income. This comprehensive guide is designed to help company drivers and owner-operators navigate the mortgage qualification process, maximize their eligible income, and secure the keys to their dream home.

Why Truck Drivers Face Unique Challenges Getting a Mortgage

When a standard 9-to-5 employee walks into a big retail bank for a mortgage, the loan officer simply looks at their W-2 and recent pay stubs. For truck drivers, the financial picture is rarely that simple. Underwriters (the people who approve your loan) are trained to look for steady, predictable income. Trucking income, by its very nature, can be variable. Here are the most common hurdles truck drivers face:

- Complex Pay Structures: You might be paid by the mile, by the load, by the hour, or a combination of all three. You may also receive safety bonuses, layover pay, or detention pay.

- Per Diem Allowances: Many company drivers receive non-taxable per diem pay to cover meals and incidental expenses while on the road. Because this income is not taxed, big banks often exclude it from your qualifying income, making it look like you earn less than you actually do.

- Employment Status Changes: It is common in the trucking industry to switch from being a W-2 company driver to a 1099 owner-operator. Lenders typically require a two-year history in the same employment type.

- Massive Tax Write-Offs: Owner-operators run a business. To lower your tax burden, you write off fuel, maintenance, insurance, depreciation on your truck, and travel expenses. While this is great for your tax bill, it drastically lowers your “net income”—which is the number traditional lenders use to qualify you for a mortgage.

How Your Employment Type Impacts Your Home Loan

The first step in your mortgage journey is identifying how the IRS and mortgage lenders classify your income. The documentation you need and the loan programs available to you will depend heavily on whether you are a W-2 company driver or a 1099 owner-operator.

Company Drivers (W-2 Employees)

If you drive a company truck and receive a W-2 at the end of the year, your mortgage process will be closer to a traditional loan application. However, because your income might fluctuate based on the routes you take or the miles you drive, lenders will typically average your income over the last 12 to 24 months. If your income has been increasing, this works in your favor. If your miles dropped last year, the lender will want to know why.

Owner-Operators and Independent Contractors (1099 / Self-Employed)

If you own or lease your rig and operate as an independent contractor, mortgage lenders view you as self-employed. This means you will face stricter documentation requirements. Standard loan programs will require two years of personal and business tax returns. The underwriter will look at your net income (after all those heavy deductions). If your net income is too low to qualify for the home you want, do not panic—there are specialized loan products, such as Bank Statement Loans, designed specifically for self-employed professionals like you.

Comparing Mortgage Qualification: W-2 vs. 1099 Truck Drivers

| Feature | Company Driver (W-2) | Owner-Operator (1099 / Self-Employed) |

|---|---|---|

| Income Calculation | Base pay, mileage, bonuses, and grossed-up per diem (averaged over 2 years). | Net business income after tax deductions (or 12–24 months of bank statement deposits). |

| Required History | Typically 2 years in the trucking industry (exceptions can be made for recent CDL school grads). | Strictly 2 years of self-employment history as an owner-operator. |

| Tax Deduction Impact | Minimal impact. Gross income is typically used. | High impact. Heavy write-offs reduce qualifying income on traditional loans. |

| Primary Documents Needed | Last 2 years of W-2s, 30 days of pay stubs, 2 months of bank statements. | Last 2 years of tax returns (or 12–24 months of business bank statements), business license/incorporation docs. |

Understanding Per Diem Pay and Mortgage Qualification

One of the biggest frustrations for company drivers is how lenders treat per diem pay. Per diem is a daily allowance given to you by your employer to cover meals and lodging. Because the IRS does not tax this money, it does not show up as taxable income on your W-2.

Inexperienced loan officers will look at your W-2, see a lower number, and tell you that you do not qualify for the home you want. As a Certified Mortgage Consultant® serving the Portland and Vancouver metro areas, I know how to handle per diem income.

Depending on the loan program (such as conventional Fannie Mae or Freddie Mac loans, or government-backed FHA and VA loans), we can often gross up your non-taxable per diem income. Because you do not pay taxes on this money, it is actually worth more than standard income. Lenders allow us to multiply your per diem income by 1.15 or 1.25 (a 15% to 25% increase) and add it back into your total qualifying income. This strategy can significantly increase your purchasing power and help you get approved for a larger loan amount.

Best Loan Programs for Truck Drivers in Oregon, Washington, and Idaho

There is no “one-size-fits-all” mortgage. As an independent mortgage broker, I have access to dozens of lenders and hundreds of loan products. This allows me to match your specific financial profile with the right mortgage program. Here are the best options for CDL professionals:

1. Conventional Loans

Conventional loans are great for truck drivers with strong credit scores (typically 620 or higher) and a solid two-year employment history. They offer competitive interest rates and require as little as 3% down for first-time homebuyers. If you have been a W-2 driver with consistent mileage and per diem, a conventional loan is often the most cost-effective route.

2. FHA Loans

Backed by the Federal Housing Administration, FHA loans are incredibly forgiving. They require a minimum down payment of just 3.5% and are ideal for truck drivers who might have a few dings on their credit report or higher debt-to-income (DTI) ratios. FHA loans are also very flexible when it comes to averaging fluctuating trucking income.

3. VA Loans for Military Veteran Truckers

A significant number of truck drivers are military veterans. If you have served in the US Army, Marine Corps, Navy, Air Force, Coast Guard, or National Guard, you may be eligible for a VA loan. VA loans offer $0 down payment, no private mortgage insurance (PMI), and highly competitive interest rates. We can easily verify your VA eligibility and use your trucking income to qualify you for this outstanding benefit.

4. Bank Statement Loans (Non-QM) for Owner-Operators

If you are an owner-operator who writes off a large portion of your income to save on taxes, traditional loans might reject you. Enter the Bank Statement Loan. Instead of looking at your tax returns, the underwriter will review 12 to 24 months of your business or personal bank statements. They will calculate your income based on the total deposits (freight payments) coming into your account, minus a standard expense factor. This allows self-employed truckers to prove their true cash flow and buy a home without having to amend their tax returns to show a higher net profit.

The Truck Driver’s Mortgage Checklist: What You Need to Apply

Because you spend most of your time on the road, gathering paperwork can be difficult. The key to a smooth, stress-free mortgage process is to get your documents organized before you apply. Keep this checklist handy in your cab:

- Identification: A valid driver’s license (your CDL) and Social Security card.

- Proof of Income (W-2 Drivers): The last two years of W-2 forms and your most recent 30 days of pay stubs. Ensure your pay stubs clearly show your mileage rates, base pay, and any per diem.

- Proof of Income (Owner-Operators): The last two years of personal and business tax returns (all pages and schedules), or 12 to 24 months of complete business bank statements if applying for a Non-QM loan.

- Asset Verification: The last two months of personal bank statements to prove you have the funds for your down payment and closing costs. Be prepared to source any large, unusual deposits.

- Employment History: A two-year history of your employers, including contact names and phone numbers for HR departments so we can verify your employment.

- CDL Documentation: If you recently graduated from a CDL training program and have less than two years of work history, provide your graduation certificate. Some lenders will count your schooling toward your two-year employment history requirement.

Step-by-Step Mortgage Process for CDL Professionals

Buying a home while driving across the country might sound impossible, but modern technology and a dedicated mortgage broker make it highly convenient. Here is how we structure the process for busy truck drivers:

Step 1: The Remote Strategy Session

You do not need to come into a Portland office to get started. I offer flexible Zoom Strategy Sessions and phone consultations that can be scheduled around your routes, breaks, or layovers. We will discuss your goals, your pay structure, and your timeline.

Step 2: Digital Pre-Approval

Step 3: House Hunting

With your pre-approval in hand, you can start shopping for homes in Portland, Beaverton, Vancouver, or anywhere in Oregon, Washington, and Idaho. Whether you are looking for a single-family home with RV parking for your rig, or a low-maintenance condominium, you will shop with confidence.

Step 4: Underwriting and Appraisal

Step 5: Closing Day

When your loan is “Clear to Close,” you will sign the final paperwork. If you are out of state on a long haul, we can often arrange for a mobile notary to meet you wherever you are, ensuring your closing stays on track without disrupting your work schedule.

Actionable Tips to Protect Your Mortgage Approval

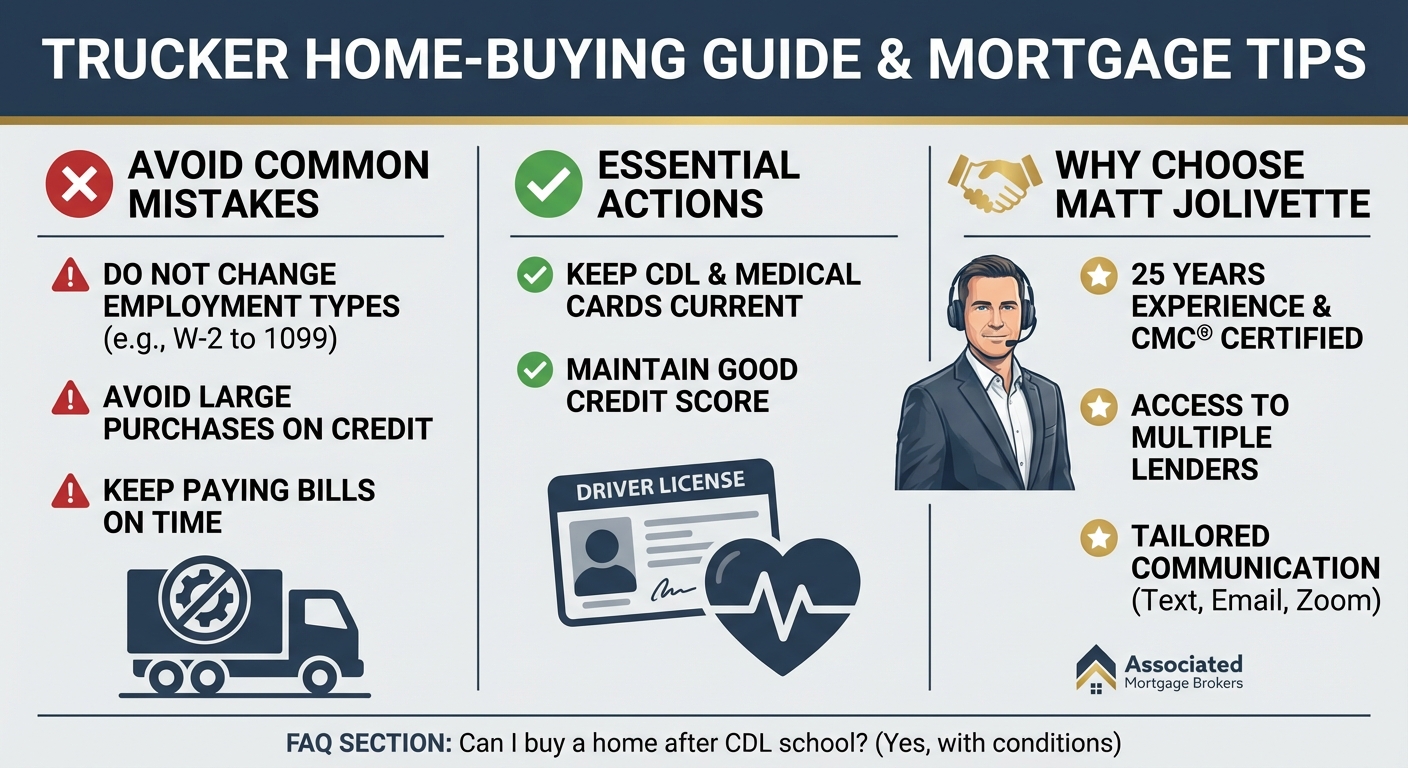

- Do Not Change Employment Types: The biggest mistake a trucker can make during the home-buying process is switching from a W-2 company driver to a 1099 owner-operator. This resets your employment history clock and can instantly kill your mortgage approval. Wait until after you have the keys to your new home to start your own trucking business.

- Keep Your CDL Current: Ensure your commercial driver’s license and medical cards do not expire while you are in the underwriting process.

- Avoid Large Purchases: Do not finance a new personal vehicle, buy expensive furniture on credit, or co-sign a loan for anyone. This changes your debt-to-income ratio and can cause your loan to be denied at the last minute.

- Keep Paying Your Bills on Time: A single late payment on a credit card or auto loan can drop your credit score significantly, potentially changing your interest rate or disqualifying you entirely.

Why Choose Matt Jolivette as Your Local Portland Mortgage Broker?

When you are navigating the complexities of trucking income, you cannot afford to work with an inexperienced call-center lender who treats you like just another file number. You need a local expert who understands the Pacific Northwest housing market and the intricacies of self-employed and non-traditional income.

Here is why truck drivers across Oregon, Washington, and Idaho trust me with their home financing:

- 25 Years of Experience: I have been a licensed Mortgage Broker since 2000. I have seen every type of trucking pay structure and know exactly how to present your file to an underwriter for a fast approval.

- Certified Mortgage Consultant® (CMC®): Less than 1% of mortgage brokers hold this prestigious designation. It represents the highest level of education, ethics, and expertise in the mortgage industry.

- Access to Multiple Lenders: Because Associated Mortgage Brokers is an independent firm founded in 1989, I do not work for a big bank—I work for you. I shop multiple wholesale lenders to find the lowest interest rates and the best loan programs for your specific situation.

- Tailored Communication: I know you cannot always answer the phone at 2:00 PM on a Tuesday. I offer flexible communication via email, text, and Zoom to accommodate your driving schedule.

Frequently Asked Questions (FAQs) for Trucker Mortgages

Can I buy a home if I just graduated from CDL school?

Yes, it is possible. While most lenders prefer a two-year employment history, many will count your time in an accredited CDL training program toward that requirement. As long as you are currently employed as a W-2 driver and have a steady income, we can often secure an approval.

Do I need a 20% down payment to buy a house?

Absolutely not. That is a common mortgage myth. If you are a military veteran, you can buy a home with 0% down using a VA loan. FHA loans require just 3.5% down, and some conventional loans require only 3% down for first-time homebuyers. We can also explore down payment assistance programs if you qualify.

What if my credit score is less than perfect?

Life on the road can make managing mail and bills difficult, and sometimes credit scores take a hit. I work with lenders who accept credit scores as low as 620 (and sometimes lower for specific government loans). If your score needs improvement, I can provide a strategic plan to help you boost your credit before you apply.

Can I use my trucking income to buy an investment property?

Yes. If you already own a primary residence and want to build wealth through real estate, you can use your trucking income to qualify for investment properties or multi-family homes (like duplexes or fourplexes). We also offer Debt Service Coverage Ratio (DSCR) loans for investors, which qualify the loan based on the property’s rental income rather than your personal trucking income.

Ready to Park Your Rig in Your Own Driveway?

Stop paying rent and start building equity. Whether you are a first-time homebuyer looking to put down roots in Portland, an owner-operator wanting to upgrade to a property with acreage in Idaho, or looking to refinance your current home in Washington to consolidate debt, I am here to guide you every step of the way.

Your hard work keeps the country moving. Let my hard work get you into the home you deserve. The mortgage process does not have to be stressful when you have the right advocate in your corner.

Take the first step today:

- Call or text me directly at (503) 545-8843

- Send an email to matt@associatedmortgage.com

- Or, start your journey immediately by completing my secure online questionnaire to request a quote.

Compliance & Legal Disclaimers

Matt Jolivette, CMC® | Mortgage Broker | Licensed in Oregon, Washington, and Idaho | NMLS#: 90661. Associated Mortgage Brokers is a privately owned mortgage broker firm in Portland, Oregon. This page is for informational purposes only and does not constitute a commitment to lend. All loans are subject to credit and property approval. Interest rates, program terms, and conditions are subject to change without notice. Not all products are available in all states or for all amounts. Veterans and active US military may be eligible for a $0 down VA loan (not applicable for refinances). Contact Matt Jolivette for full program details and to verify your eligibility.